Avoiding the venture trap

This is the 2nd essay in a 5-part series on funding models for the creator economy

- Funding the creator economy

- Avoiding the venture trap

- Cash rules everything around me

- Shared income and bespoke finance

- NFTs, $GME, and the crowdfunded Cambrian explosion

Venture capital is the shiniest of the capitals. You, the founder, get a big check at an eye-popping valuation. TechCrunch writes an article saying you are the coolest kid on the block. Your mom is proud. And if the whole thing goes belly-up, you just walk away debt-free.

I am not here to tell you not to take that deal. In fact, I spent six years working at a venture-backed company and I have invested in over 30 companies on traditional venture-style terms. I am not anti-VC! But I do want to share why you might not want that deal and why alternatives might be a better fit for you, particularly if you want to build independently online.

Why venture capital might not be for you

Much virtual ink has been spilled on why not to raise VC, so I'll stick to a brief summary of the highlights:

- With the incredible leverage individuals can get from cheap online software (what Tyler Tringas calls the Peace Dividends of the SaaS Wars), you probably don't need a large chunk of capital to get started.

- VCs want your business to go to the moon or die quickly so they can move on to other bets. If you want something a little less bimodal, your values aren't strongly aligned.

- The venture model takes permanent partial ownership of your company in exchange for an investment. People compare it to getting married. If you'd prefer to maintain long-term ownership and control of your company, consider alternatives. This is particularly problematic for individual creators with diverse revenue streams. What does it even mean to own 10% of a creator? Doesn't sound good.

- Most companies in most industries are not going to be unicorns. The early days of tech were defined by huge, winner-takes-all global markets: search, social media, smartphones, silicon chips. Now, we are entering the deployment phase of the information revolution, where software is replacing existing systems in essentially every industry. Everything from bingo card creation to niche newsletters can be profitable businesses—just not venture backed ones.

The astute reader will notice that while people have been talking about these reasons for years, all of them are becoming much more true. There will always be bloody, monopolized multi-billion dollar markets that make sense for VC. But increasingly, new markets will be niches. Venture capital is a particularly bad solution for the online creators, solopreneurs, and indie developers that play well in these niches.

Misaligned incentives

If this is whole creator economy thing to be a big deal, why doesn't venture capital change to fit the needs of these groups? It can't. While venture capital will undoubtedly help create some of the biggest platforms of the creator economy, it has no business funding indie companies. I mean that literally.

Indie.vc, the leading innovative model for startup funding, called it quits last week. While it's a sad set-back for alternative funding models, there was something peculiar about the announcement. These two sentences stood out to me:

I have no doubt that in 4–5 years we’ll see our Indie companies posting comparable results as our previous funds that have generated 5x+ net multiples for our LPs.

[indie.vc] cost us 80% of our LP base. Unfortunately, as we’ve sought to lean more aggressively into scaling our investments and ideas behind an “Indie Economy” we’ve not found that same level of enthusiasm from the institutional LP market.

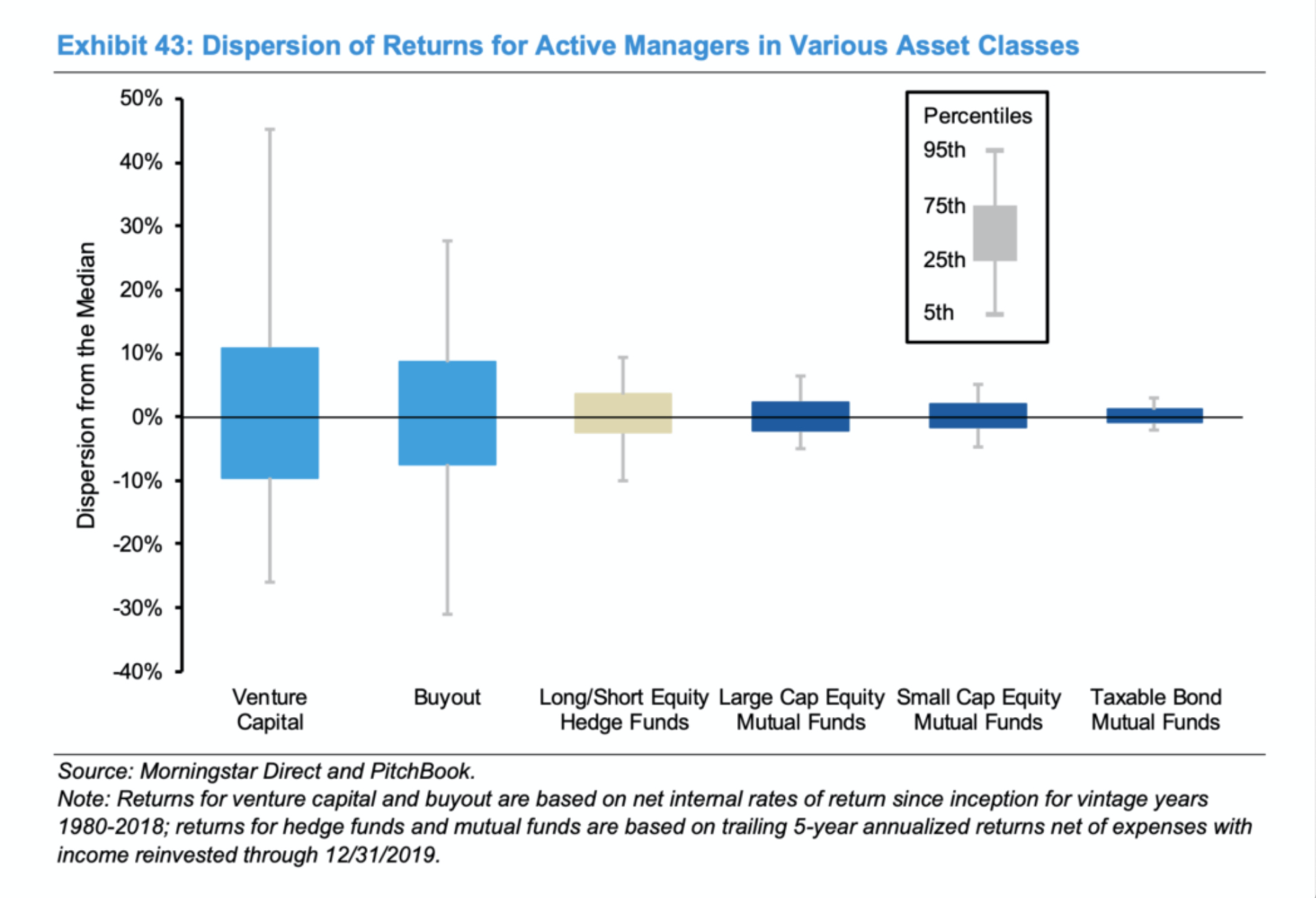

Wait, a second. If Indie has helped great companies generate solid returns, why did they lose 80% of their investors? The answer to that question gets at the heart of venture capital: it doesn't exist because startups need it, it exists because large investors (LPs) need high-risk portfolio allocations.

A fundamental premise of portfolio management is risk allocation. You want most of your assets in relatively safe investments and a small percentage of your assets in high risk investments. If the high-risk investments tank, you lose a couple percentage points of returns. But if they succeed, they can return more money than all of the other asset types. Low downside risk, high upside potential.

This chart shows why large pension funds and private equity firms need to have VC allocations to stay competitive:

Venture capital has been a tremendously useful tool for fulfilling this need (and creating a huge consumer surplus in the form of hundreds of large tech companies). It's a perfect asset class for solving a particular problem in portfolios & creating some incredible things that wouldn't otherwise exist. But it is not a one-size-fits-all funding model. It is designed for outliers—in other words, not most businesses!

Alternatives

The greatest trick venture capital ever pulled was convincing the world other funding models didn't exist. When people talk about fundraising in the context of startups, they almost always mean selling equity to venture capitalists.

But when I say "funding model" I am generally not talking about who you raise money from. Venture capitalists, angel investors, incubators, syndicates, friends & family rounds — ultimately, these are all the same dilutive equity-based funding model, just raised from different groups of investors. I am talking about the financial structure of the fundraise.

The remaining three essays in this series cover the major categories of these alternative financial structures: